Research & Development Tax Credit

A dollar-for-dollar reduction in tax liability for the work you already do — with no caps, no application fees, and no restrictions on how you use the credit.

Your Business Is Already Taking the Risk

Every day, your business is taking a risk. Whether you're researching a new drug, creating a mobile app, refining a mold or building a skyscraper, you're doing more than just running a business. You're taking a leap of faith that doesn't guarantee you'll get paid for your hard work. That's why the Research & Development (R&D) tax credit exists.

The Tax Benefits Are Significant

Remember the Eighties

It started back in 1981, when President Reagan enacted the Research & Experimentation tax credit to reboot American manufacturing. It has since grown into an estimated $12 billion credit that helps more than 12,000 American businesses compete in a complex global economy.

On December 15, 2015, the R&D tax credit was cemented as a permanent provision of the IRS tax code, with two major changes that expanded access for small businesses: companies with less than $50 million in gross receipts can use the credit to offset AMT, and start-ups with no income tax liability can apply credits to payroll tax — a savings of up to $250,000 a year.

The 2017 Tax Cuts and Jobs Act went further, repealing the corporate AMT and permanently reducing the C-Corp tax rate from 35% to 21% — increasing the net value of R&D credits by more than 21%.

Estimated R&D tax credits provided to U.S. businesses (in billions).

How the R&D Tax Credit Works

The R&D tax credit provides an actual credit on the taxes you pay — one of the most valuable available because it is a dollar-for-dollar reduction in tax liability. There are no caps, no application fees, and no restrictions on how you use your credit dollars. Laboratories and high-tech firms are obvious candidates, but architectural, engineering, software and many manufacturing companies are also eligible.

Manufacturing+

- Aerospace

- Apparel & Textiles

- Automotive

- Building Systems Control

- Chemical

- Electronics

- Firearms & Ammunition

- Food & Consumer Packaged Goods

- Foundries

- Job Shops

- Life Sciences

- Medical Equipment

- Metals

- Oil & Gas

- Plastics

- Telecommunications

- Tool & Die

Architecture, Engineering & Construction+

- Civil Engineering

- Electrical Engineering

- Electrical Contracting

- Environmental Engineering

- Mechanical Engineering

- General Contracting

- Product Engineering

- Structural Engineering

- Mechanical Contracting

Software+

- Accounting & Financial Software

- Enterprise Infrastructure Software

- ERP Software

- Logistics Management Software

- Document Management Systems

- Claims Processing Software

- Educational Software

- CRM Software

- Content Management Software

- Database Management Software

- Video Games & Game Creation

- Medical & Healthcare Management Software

Other Industries+

- Agriculture / Farming

- Brewing

- Distilled Spirits

The Four-Part Test

Whether an activity qualifies for R&D is based on a broad set of definitions known as the Four-Part Test. It is our job to substantiate, document and prove the portion of your business activity that involves R&D.

Qualified Purpose

The activity must aim to create a new or improved business component — a product, process, technique, formula, invention, or piece of software — that improves function, performance, reliability, or quality.

Elimination of Uncertainty

The activity must be intended to discover information that eliminates uncertainty about the capability, method, or appropriate design of developing or improving the business component.

Process of Experimentation

Substantially all of the activities must involve a process of experimentation — evaluating alternatives through modeling, simulation, systematic trial and error, or other methods.

Technological in Nature

The process of experimentation must rely on the principles of a hard science such as engineering, physics, chemistry, biology, or computer science.

Qualified Research Expenses (QRE)

The QRE is the basic unit of the R&D tax credit, derived from salaries, supplies and contractor expenses. About 80 percent of the credit you receive comes from salaries. As part of the study, we determine whether an activity counts toward R&D, the employees involved, what you pay them, and the portion of their time dedicated to that activity — which is why payroll data is essential to a proper calculation.

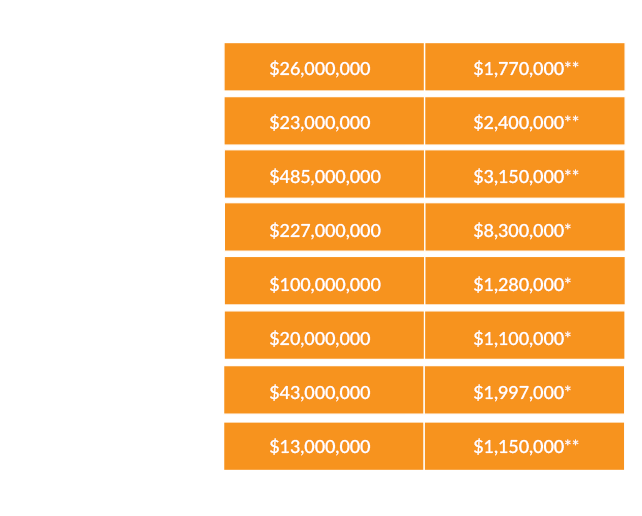

How Much Is the R&D Tax Credit Worth?

The size of the credit varies because it depends on the amount of R&D activity that can be quantified. Across our client base, the average federal R&D tax credit in a single year is approximately 1% of a company's annual revenues. Credits can be claimed retroactively for up to three years — and 36 states provide an additional R&D credit on top of the federal benefit.

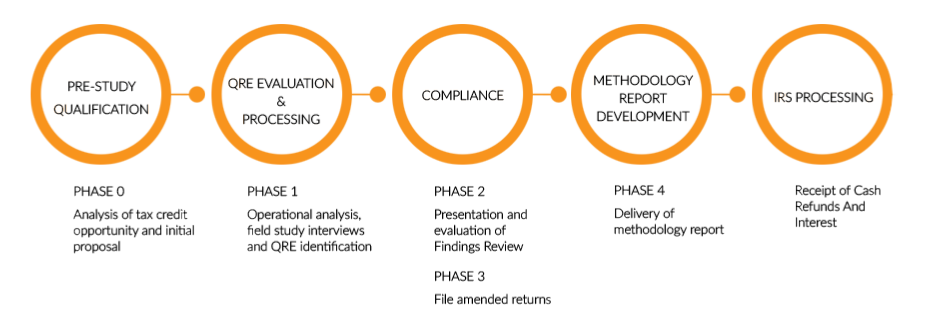

The Apex Advisors R&D Tax Credit Process

We use a comprehensive process that ensures every possible R&D activity is considered and calculated with accuracy. The Preliminary Assessment is provided to companies at no cost, and the estimated duration of all phases is two to three months.

- 1Preliminary Assessment (complimentary)

- 2Qualification of activities & employees

- 3Quantification using our PAD method

- 4Documentation & substantiation

- 5Filing & audit-ready deliverables

Request a Complimentary Estimate

See what your R&D activity could be worth — at no cost.