IC-DISC Exporter Tax Benefit

A federal incentive that lets U.S. manufacturers, producers, resellers and exporters convert a portion of export income into lower-taxed qualified dividends.

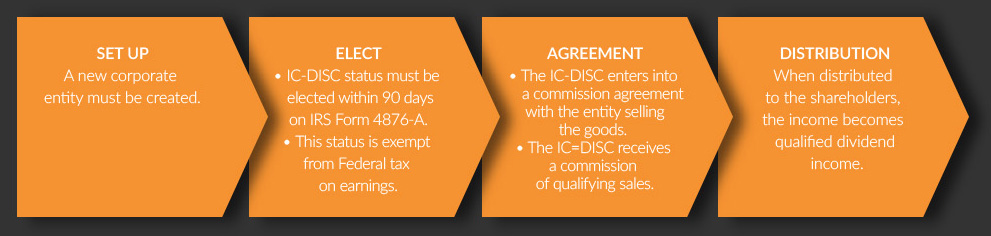

IC-DISC is a tax incentive for manufacturers, producers, resellers and exporters of goods produced in the United States. To reduce taxable income, a company can create an Interest Charge Domestic International Sales Corporation (IC-DISC) — a separate corporation that acts as a sales commission agent. Based on their foreign sales, exporters pay a commission to the IC-DISC and then deduct it from ordinary business income, resulting in a deduction at ordinary tax rates. The IC-DISC receives the commission without paying federal tax on the income.

Who Is Eligible?

Any entity — including C corporations, S corporations, partnerships, LLCs and sole proprietors — that sells “export property” and is profitable can benefit from an IC-DISC. Section 993(c) defines export property as property that is:

- Manufactured, produced, grown, or extracted in the United States;

- Held for sale, lease, or rental for direct use, consumption, or disposition outside the United States; and

- Has a fair market value not more than 50% attributable to articles imported into the United States.

Qualified Candidates Include

- Companies that directly export goods they manufacture.

- Companies that provide architectural or engineering services performed in the U.S. for a building or bridge built outside the U.S.

- Companies that manufacture a good that is included in a product that is exported.

The IC-DISC Process

Request a Complimentary Estimate

Find out how much an IC-DISC could save your export business.